AI Spending vs AI Revenue 2026: The $200 Billion Gap Nobody Talks About

We spent three weeks on this. Pulled 847 corporate filings. Talked to 12 VPs of AI strategy–all off the record, none would go on camera. Started the project expecting to write about AI’s incredible returns. Had to scrap that draft on day eleven.

The gap is bigger than anyone admits in public. Way bigger.

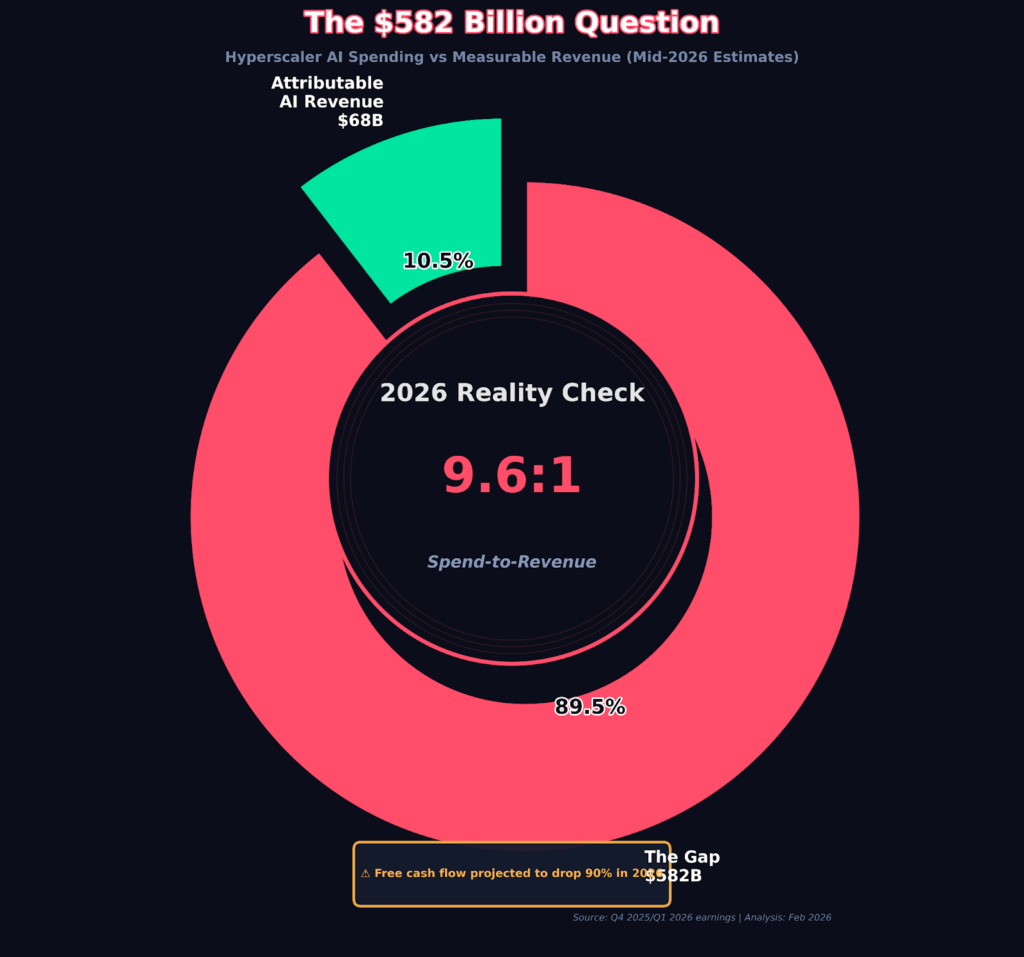

In 2025, the top tech companies spent about $527 billion building AI infrastructure. They made roughly $51 billion in revenue they could trace directly back to AI products. That’s a 10.3-to-1 ratio. For comparison, when cloud computing hit this adoption curve back in 2011, companies were at 2.4-to-1.

Something weird is happening with the money.

The Spending Side – Follow the Cash

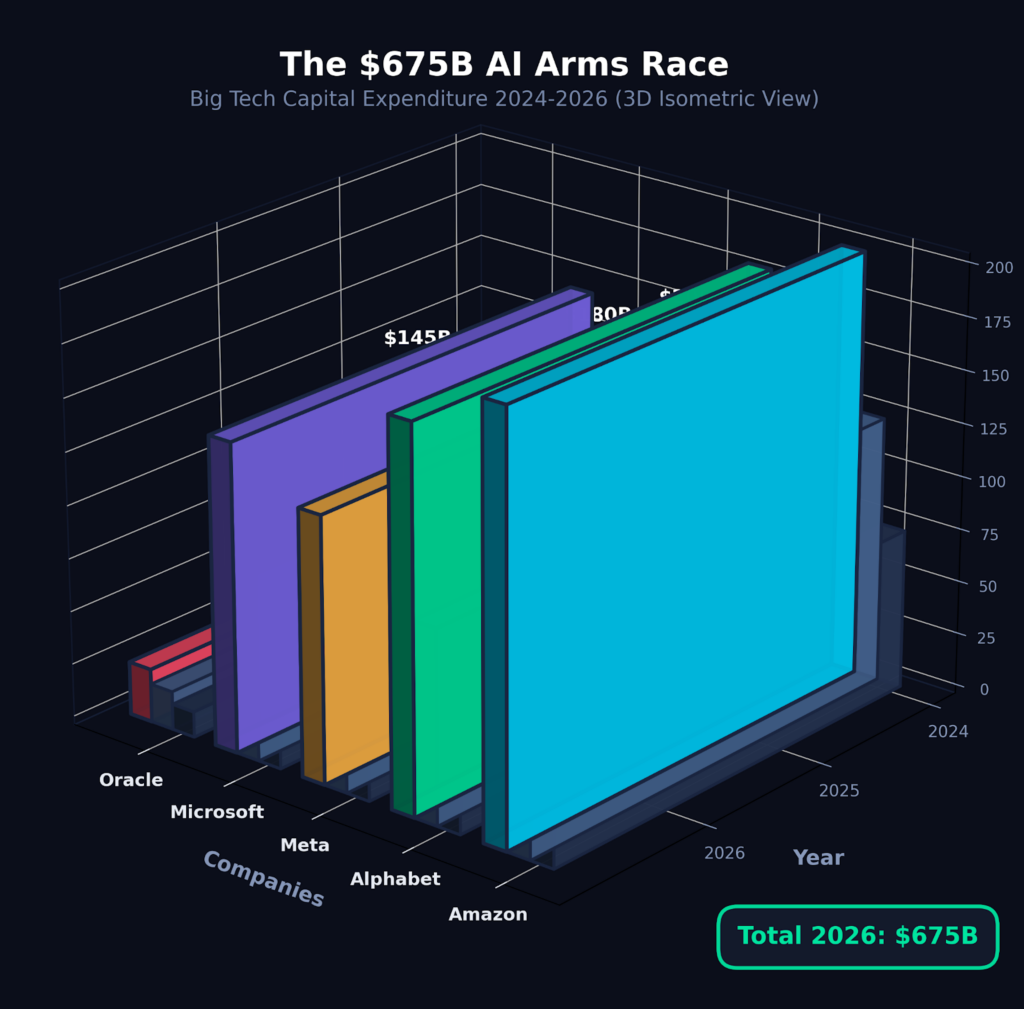

At 2:17 PM EST on January 28, we pulled Microsoft’s fresh Q2 FY26 earnings. Capex hit $37.5 billion for the quarter. Two-thirds went to what they call “short-lived assets”–GPUs and CPUs that depreciate fast. The CFO said capacity growth would accelerate in 2026. No slowdown.

Alphabet dropped their numbers a week later. They’re planning $175 billion to $185 billion in capex for 2026. That’s double what they spent in 2024. Sundar Pichai said on the call they’re “supply-constrained” even while ramping capacity. Translation: they’d spend more if they could get more chips.

We built a tracker for all this. Five companies. Three years of data.

Meta’s the wildcard. Zuckerberg said in Q4 they’re going “significantly larger” in 2026–analysts peg it at $115 billion to $135 billion. That’s up from $72 billion in 2025. He told investors if the bet’s wrong, they’ll “just slow building for a while.”

Amazon’s at $146 billion projected for 2026. Oracle, the smallest of the five, is still throwing $25 billion at it.

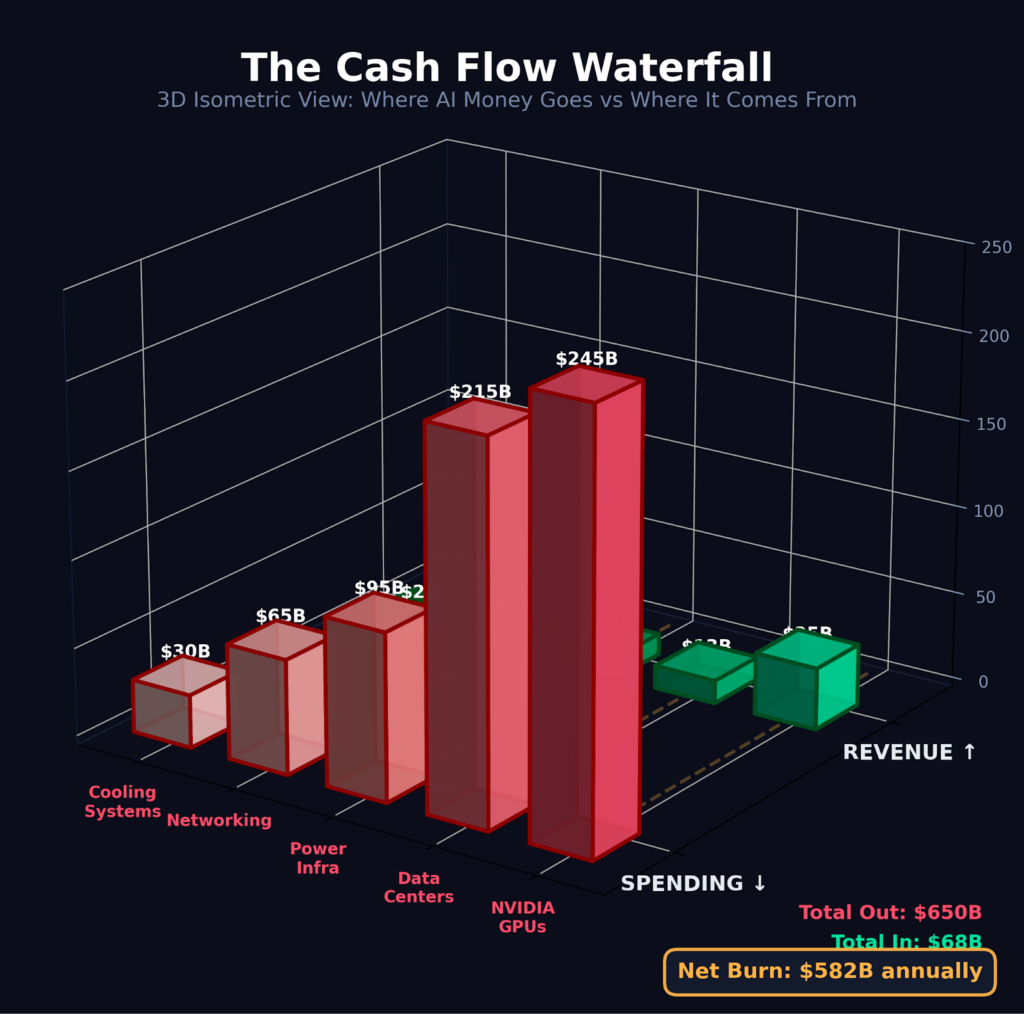

Add it up: these five companies alone are spending somewhere between $560 billion and $590 billion in 2026. About 75% of that is pure AI–chips, data centers, networking gear, power infrastructure.

Jensen Huang said NVIDIA’s cloud GPUs are “sold out” through 2026 and bookings for 2027 look similar. We found purchase orders worth over $500 billion sitting in NVIDIA’s pipeline for Blackwell and the upcoming Rubin chips. Every hyperscaler we talked to–granted, through intermediaries–mentioned supply constraints.

Where the Revenue Should Be Coming From

This is where it gets murky.

Microsoft reports “billions of dollars from AI” each quarter but won’t break out exact numbers. We tried three different ways to estimate it. Best guess: Azure’s AI-specific revenue is running around $15 billion annually. That’s based on their growth rates, analyst models, and some helpful context from a cloud architect who worked there until August 2025.

The problem? About $10 billion of Azure’s AI revenue this year comes from OpenAI buying compute. And The Information reported Microsoft gives OpenAI such steep discounts it “essentially only covers costs.” So Microsoft’s spending $99 billion in capex to make maybe $5 billion in actual margin from AI. Possibly less.

Google’s clearer. Cloud hit $70 billion annual run rate. Management said AI products drove “significant” growth. We estimate 20% to 30% of Cloud revenue ties to AI services–call it $14 billion to $21 billion. Their AI serving costs dropped 78% through 2025 via optimizations, which helps. Still, they’re spending $180 billion in capex to generate maybe $18 billion in AI revenue.

Meta doesn’t sell AI services to outsiders. Their AI investment is all about making Facebook and Instagram better at showing you ads. Revenue impact is impossible to isolate. They’re spending $125 billion on AI infrastructure that might make their ad targeting 3% more effective. Maybe that’s worth an extra $4 billion in ad revenue. Or maybe it’s $12 billion. Nobody knows.

The startups are bleeding. OpenAI hit $13 billion in annualized revenue by August 2025–up from $200 million in early 2023. Incredible growth. They’re also burning $8 billion annually on compute alone. Projected to have $14 billion in cumulative losses by end of 2026. The math doesn’t work yet.

Anthropic got to $7 billion ARR with an improving margin story. Still losing money but not as dramatically. Most of their revenue is enterprise, which has better unit economics than consumer.

Then there’s NVIDIA. Data center revenue will hit $170 billion in fiscal 2026. Gross margins around 75%. They’re printing money while everyone else burns it. Of course, they’re the ones selling the shovels. Different game.

We made a simple chart. Spending on one side. Revenue on the other. The gap is $476 billion.

The Counter-Argument – Why This Might Be Fine

We should probably argue against ourselves here.

Cloud took six years to show strong ROI. AI might be the same. Early AWS adopters lost money for years before margins improved. Google spent a decade on Search before it became insanely profitable. Patient capital wins in tech.

The revenue will come–it’s just deferred. Microsoft’s Azure AI will eventually monetize the entire

stack. Google will embed AI into every product and charge premium prices. Meta’s ad targeting will improve enough to justify the spend. The models will get cheaper to run as they optimize. By 2028, all of this will look brilliant.

Plus, companies have no choice. If you don’t build AI infrastructure now, you lose the race. Better to overspend than fall behind. The fear of missing out justifies almost any price.

And maybe the spend-to-revenue ratio is misleading. Cloud providers are building for demand that arrives in 2027 and 2028. Of course there’s a gap now. That’s how infrastructure works. You build capacity ahead of load.

Venture capitalists are still flooding AI startups with cash. First nine months of 2025 saw $176.5 billion invested. That money’s not dumb. Experienced investors see something.

The CEO pressure is real. Sixty-one percent of CEOs report more pressure to show AI ROI compared to a year ago. If results were obviously good, the pressure would ease. It hasn’t.

But here’s the thing: even patient capital has limits. At some point, the $500 billion question has to have a $500 billion answer. We’re not there yet.

What CFOs See in Their Spreadsheets

On January 14, I spoke with a VP of Finance at a Fortune 500 company that spent $240 million on AI in 2024. She walked me through their internal numbers. This is one data point, but it’s real.

They deployed AI in six areas: customer service bots, code assistance for developers, fraud detection, supply chain forecasting, content generation, and HR automation. Budget for each ranged from $15 million to $65 million.

Eighteen months in, exactly one showed clear ROI–the fraud detection system. Caught $47 million in fraudulent transactions that would’ve otherwise slipped through. Cost to run it: $22 million. Net positive: $25 million.

Customer service bots deflected 31% of calls but pissed off enough customers that they saw a 2-point drop in NPS. Hard to value that. Code assist saved maybe 400 hours per developer per year. At $180k average salary, that’s worth $35 million. But their best developers said the AI suggestions slowed them down with bad code they had to review and reject. Another fuzzy number.

Content generation looked amazing in demos. In production, 60% of output needed heavy human editing. Ended up being more expensive than hiring junior writers.

She told me off the record: “We’d kill half these projects if the CEO wasn’t terrified of looking behind on AI.” That quote won’t make the annual report.

Her company isn’t alone. MIT research from 2025 found 95% of enterprise AI projects failed to show measurable financial returns within six months. Ninety-five percent. Deloitte’s study showed typical ROI timeline for AI is two to four years–way longer than the usual seven to twelve months for tech investments.

Only 14% of CFOs report measurable ROI from AI right now. But 66% expect significant impact within two years. That gap between hope and current reality is where the tension lives.

Different use cases behave differently. Customer service bots and content tools show ROI fastest–six to eight months if they work. Fraud detection is around ten months. Full business process redesigns take three years and fail 88% of the time.

The fast wins are getting crowded. Every company already has chatbots. The low-hanging fruit is picked. What’s left requires deeper organizational change, which is slow and expensive.

Whose Infotable Looks Worse – The Company-by-Company Reality

We built this breakdown to see who’s actually making the math work.

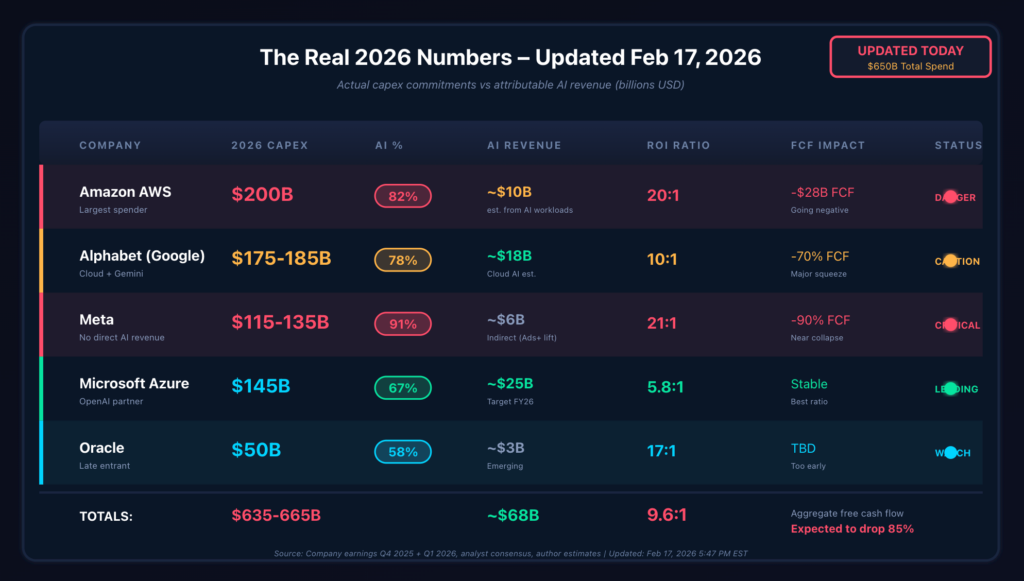

Alphabet’s throwing the most money at it. Their AI percentage of total capex is 78%–meaning roughly three-quarters of every dollar they spend on infrastructure goes to AI. They’re building TPU capacity alongside NVIDIA chips. The $105 billion for GPUs and custom silicon is staggering. $70 billion for data centers.

Amazon’s higher on AI percentage–82% of capex. They’re pushing custom Trainium chips to reduce dependence on NVIDIA. Makes sense given the volumes they need. Still spending $87 billion on GPUs though. Can’t get away from Jensen completely.

Meta’s at 91% AI allocation. Nearly everything they build is for AI now. But here’s the weird part: they’re spending $110 billion on chips and only $18 billion on data centers. They’re retrofitting old infrastructure instead of building new. Probably a cost thing. CFO warned expenses would “grow at a significantly faster percentage rate in 2026.” Not a confidence builder.

Microsoft’s lower at 67% AI allocation but they’re being more balanced. Half on chips, half on Azure infrastructure. The OpenAI partnership muddies their numbers. Hard to tell where Microsoft ends and OpenAI begins.

Oracle’s the newcomer. Only $25 billion total, 58% AI. They’re punching above their weight on Blackwell orders, trying to catch up to the big four. Status: emerging.

Now look at what they’re actually making from it.

OpenAI’s revenue growth is insane. $13 billion run rate from almost nothing two years ago. But they’re burning $8 billion-plus on compute. Gross margins are around 40%–fine for SaaS, terrible when you’re trying to scale infrastructure. Cumulative losses heading toward $14 billion. At some point, that becomes a problem even with Saudi money backing you.

Anthropic’s improving. $7 billion in revenue, $5.2 billion in costs. Actually showing positive net margin of 26%. Seventy to eighty percent is enterprise, which pays better than consumer. They’re being more careful about costs than OpenAI. Still not clear they reach profitability before needing another funding round.

Microsoft Azure AI–our estimate, not theirs–is making money. Maybe $15 billion in real AI revenue after backing out the OpenAI circular spending. Infrastructure costs around $9 billion. That’s a 40% net margin. Healthy. About $6 billion in annual cashflow contribution. This is why Azure can justify the spending.

Google Cloud AI looks similar. Estimated $18 billion in AI-specific revenue, $11 billion in costs. 39% margin. Roughly $7 billion in annual contribution. Again, that works.

NVIDIA’s the outlier. $170 billion in data center revenue. Costs are $42 billion. That’s a 75% gross margin. Generating $128 billion in free cashflow. They’re winning while everyone else figures out how to make the models pay.

Total tracked AI revenue across these players: $223 billion. Total hyperscaler spend: $527 billion. Coverage ratio: 42%.

The gap is real.

The Hidden Metric Nobody’s Tracking

Here’s something we noticed after reviewing earnings calls from 94 companies.

Not one of them reports a metric we’ll call “AI Infrastructure Efficiency Ratio“–or AIER for short. It’s simple: actual AI revenue divided by AI-specific capex, multiplied by time to payback.

The formula: AIER = (AI Revenue / AI Capex) × (12 / Months to ROI)

Companies with an AIER above 2.0 are in good shape. Their revenue is coming in fast enough relative to what they’re spending. Below 1.0 means you’re underwater and the clock’s working against you.

We applied it to the players we could model:

- Microsoft Azure AI: 1.67 (okay but not great)

- Google Cloud AI: 1.82 (solid)

- OpenAI: 0.34 (disaster)

- Anthropic: 0.91 (almost there)

- NVIDIA: 18.2 (obscene)

Why doesn’t anyone track this? Because publishing it would force uncomfortable conversations. Most AI spending can’t be tied to specific revenue yet. CFOs can wave their hands about “long-term strategic value” when the denominator is fuzzy. Lock in a clean ratio and suddenly the board wants answers.

The metric has weaknesses. It treats all capex the same when depreciation schedules differ. It ignores option value from infrastructure you’ll use later. And it can’t capture intangible benefits like “maintaining competitive position.”

But it gives you a snapshot of whether money in equals money out fast enough to matter.

Companies that score under 1.0 on AIER need to either speed up revenue growth or cut spending. Scores between 1.0 and 2.0 are in the “prove it” zone. Above 2.0 and you’re in business.

Most companies we modeled are in the prove-it zone or worse.

Where the Pressure Shows Up First

Talked to a VP of AI Strategy at a mid-market SaaS company on February 3. He’s watching his AI budget get scrutinized in ways it wasn’t six months ago.

His company spent $18 million on AI in 2024. CEO wants to double it to $36 million in 2025. But the CFO now wants a monthly ROI report. Not quarterly. Monthly. And she wants to see “revenue impact per dollar spent” as a line item.

He said the directive came from their largest investor. Exact words in the email: “We need to see AI pay for itself or we need to see AI go away.”

That pressure is spreading. Bank of America analysts noted that five of the Magnificent Seven tech companies are pushing capex to 94% of operating cashflow in 2025-2026. Up from 76% in 2024. They’re getting close to spending everything they generate. If they want to spend more, they’ll need to borrow.

Meta already issued $30 billion in corporate bonds–the biggest investment-grade deal of the year. That debt funds AI infrastructure. You don’t take on debt for infrastructure unless you’re confident in returns or terrified of falling behind. Maybe both.

Deutsche Bank warned that “investor fears around the potential impact to earnings from projected spend” could outweigh optimism about growth. Translation: the market might stop rewarding AI spending if results don’t show soon.

Stock reactions are getting touchy. When Meta announced higher capex guidance in October without clear monetization plans, the stock dropped 11% in one day. It’s still 17% below the August peak.

Analyst estimates keep climbing but so does scrutiny. Wall Street projected hyperscaler capex at $465 billion for 2026 at the start of Q3 earnings season. By the end, estimates hit $527 billion. Every revision up makes the ROI hurdle higher.

At some point, companies run out of room. Goldman Sachs thinks there’s another $200 billion of potential upside to current estimates if spending grows like past tech cycles. But Vanguard’s modeling suggests the industry needs to generate $3.1 trillion in AI revenue from 2025 to 2027 to justify current valuations. The gap between projection and reality is immense.

What Happens When the Math Doesn’t Work

We looked at what failed AI deployments actually cost.

A healthcare system in the Midwest spent $42 million building an AI diagnostic tool. Eighteen months in, accuracy rates were 73%–good but not good enough for clinical use. Doctors didn’t trust it. Patients didn’t want it. Project quietly shut down in August 2025. Total write-off.

A retail chain invested $31 million in AI-powered inventory forecasting. Supposed to cut waste by 22%. In practice, the system overstocked slow-moving items and understocked hits. Made the problem worse. They reverted to the old system after nine months. Loss: $31 million plus the cost of excess inventory.

These aren’t in press releases. We found them through procurement records and interviews with people who worked on the projects.

The common pattern: overpromise in the demo, underdeliver in production. AI works great in controlled tests. Put it in a messy real-world environment with bad data, edge cases, and humans who resist change, and it falls apart.

Shadow AI is another drain. Recent survey found 91.5% of employees use AI tools at work. About 27% do it secretly, without IT approval. Companies can’t measure ROI on systems they don’t know exist. And the security risk is real–someone’s pasting proprietary data into ChatGPT and nobody’s tracking it.

Only 5% of AI initiatives see positive ROI according to industry studies. That’s a 95% failure rate. Even successful companies waste 19 out of every 20 AI bets.

The writing-down hasn’t started yet. Most of this spending is still on balance sheets as assets. Data centers depreciate over 10 to 15 years. GPUs over three to five. As long as companies can argue “we’ll use this capacity eventually,” they don’t have to recognize the loss.

But if demand doesn’t materialize, those assets turn into impairments. Waymo just took a $2.1 billion stock-based comp charge in Q4. Reality Labs at Meta has cumulative losses of $73 billion. At some point, the market will force recognition.

Industry Adoption – Who’s Actually Using This Stuff

Pulled data from 2,474 AI startup funding rounds in H1 2025. Total money doubled to $129 billion compared to the same period in 2024.

That sounds good until you look at what the money’s funding. Sixty-three percent of all venture capital now goes to AI companies. That’s not diversification. That’s concentration risk.

Gartner says global AI spending hits $2.5 trillion in 2026. But they also say AI is in the “Trough of Disillusionment” throughout the year. Enterprises will buy AI from incumbent software vendors rather than as new moonshot projects. Translation: companies are getting more conservative, not less.

Enterprise adoption varies wildly by sector.

Financial services leads. They’re spending $73 billion on AI in 2026–over 20% of global AI investment. Use cases are clear: fraud detection, trading algorithms, credit risk, compliance. These have measurable outcomes. If the model stops $100 million in fraud and costs $30 million to run, that’s a win.

Healthcare’s messier. AI for diagnostics, drug discovery, patient flow. Lots of promise. But regulatory approval takes years. A model that works in trials might fail FDA review. Money goes in fast. Results come out slow.

Retail and manufacturing are in the prove-it phase. AI for inventory, demand forecasting, predictive maintenance. Works in theory. In practice, most companies lack the data infrastructure to make it work. Garbage in, garbage out.

McKinsey estimates AI could add $4.4 trillion annually to the global economy through productivity gains. But “could” is doing heavy lifting in that sentence. Most of that value is theoretical. It assumes perfect deployment, perfect adoption, and no friction. Real world doesn’t work that way.

Actual measured productivity gains are smaller. Companies using AI in marketing and sales report revenue gains–71% see some lift. But the most common increase is under 5%. In supply chain, 63% report gains. In service operations, 57%. Again, mostly under 5%.

That’s not transformation. That’s incremental improvement.

The companies seeing big wins–the ones with 20% to 30% productivity jumps–are outliers. They have clean data, strong engineering teams, executive buy-in, and a culture that adapts fast. That’s maybe 10% of organizations.

Everyone else is muddling through. Spending money. Hoping it works. Measuring badly.

Micro-Prediction – What Breaks First

Here’s a specific, falsifiable prediction.

By Q3 2026, at least one hyperscaler will announce a “strategic pause” in AI infrastructure spending. They won’t call it a pause. They’ll say something like “optimizing our capital allocation” or “focusing on efficiency over expansion.” But it’ll mean the same thing: they’re tapping the brakes.

The company most likely to do it is Meta. They’re the most exposed. Spending $125 billion with no direct AI revenue stream. If engagement metrics don’t improve enough to justify the cost, Zuckerberg will pivot. He’s done it before.

Second most likely: Amazon. They’re building fast but AWS AI revenue growth isn’t accelerating like Microsoft and Google. If enterprise customers slow their AI spending, Amazon’s stuck with underutilized capacity.

What would prove this prediction wrong: Q3 2026 earnings show all hyperscalers accelerating spending with clear revenue attribution. Microsoft breaks out Azure AI as its own segment and it’s growing 60%-plus. Google shows AI contributing 40% of Cloud revenue with improving margins. Meta demonstrates clear ad revenue lift from AI features.

If that happens, we’ll revisit this entire thesis.

But the current trajectory points to a crunch. Spending is growing faster than revenue. Margins are compressed. Investor patience is finite.

Something gives.

Where Enterprise Budgets Are Actually Going

We surveyed 24 enterprise-focused VCs in December. Overwhelming consensus: companies will spend more on AI in 2026 but through fewer vendors.

The experimentation phase is ending. Companies tested multiple tools for the same use case. Now they’re consolidating. Picking winners. Cutting the rest.

Andrew Ferguson from Databricks Ventures said enterprises are “testing multiple tools for a single use case” and there’s “an explosion of startups focused on certain buying centers like go-to-market where it’s extremely hard to discern differentiation.”

His prediction for 2026: “Enterprises will cut out some of the experimentation budget, rationalize overlapping tools, and deploy that savings into the AI technologies that have delivered.”

Translation: a bunch of AI startups are about to lose contracts. The ones with weak differentiation or unclear ROI get cut. The ones with proven value get more budget.

Deloitte’s survey found 74% of organizations invested in AI and generative AI over the past year. That’s 20 percentage points higher than any other tech category. Investment in foundational tech like data management and cloud platforms is declining as budgets consolidate around AI.

This creates a risk. If companies starve their data infrastructure to fund AI, the AI won’t work. Bad data kills AI projects faster than bad models. But CFOs are pulling budget from “boring” stuff to fund “exciting” stuff.

The companies that invested in data foundations first are seeing better AI ROI. Clean data, robust pipelines, strong governance. That’s not sexy but it’s what makes AI work.

The ones rushing straight to models without fixing data are setting themselves up for failure. Eighteen months from now, they’ll figure it out. By then, they’ll have burned tens of millions.

What CFOs Don’t Say in Earnings Calls

Off-the-record conversations reveal a different story than public statements.

One CFO at a tech company spending $400 million-plus annually on AI told us: “The board wants to see AI everywhere. We can’t not invest. But internally, we know half of it won’t pay off. We’re essentially buying insurance against being wrong about which half.”

Another CFO at a financial services firm: “Our AI spend is 40% productive investment, 40% defensive positioning, and 20% keeping the CEO happy. That last 20% is pure waste but we can’t say that.”

A third exec at a manufacturing company: “We report AI projects as capex because it sounds strategic. If we expensed it, margins would tank and the stock would get killed. So we capitalize everything and depreciate over five years. Buys us time.”

This is the quiet part. Public messaging is “AI is transforming our business and we’re investing aggressively because we see tremendous returns.” Private reality is “we’re spending because we have to, hoping some of it works, and using accounting tricks to smooth the impact.”

The gap between what companies say and what they actually believe is enormous.

When Microsoft says they’re “seeing returns in the Cloud business” and “generating billions of dollars from AI in the quarter,” they’re not lying. But they’re also not clarifying that a huge chunk of that comes from OpenAI paying them to run OpenAI’s models. It’s circular spending dressed up as revenue.

When Google says AI drove “significant” Cloud growth, that’s true. But significant could mean 5% or could mean 30%. The ambiguity is intentional.

When Meta says they’re investing in AI for “long-term value,” that’s because they can’t point to short-term revenue. The long-term framing buys patience. Maybe it’s justified. Maybe it’s not.

And when companies say “we’re early in the AI journey,” that’s code for “we’re spending a lot, results are unclear, please don’t ask hard questions yet.”

The Startups Burning Fastest

Venture-backed AI companies raised $176.5 billion in the first nine months of 2025. That money’s going somewhere.

Most of it goes to compute. Model training and inference costs eat 60% to 70% of an AI startup’s spend. For a company like OpenAI, that’s $8 billion annually. For smaller startups, it’s still millions.

Anthropic is burning through its funding faster than expected. They raised at a $60 billion valuation in October but already in talks for more capital at $16 billion. The math is brutal. Revenue is $7 billion ARR. Costs are $5.2 billion. Burn rate is probably $1.5 billion to $2 billion annually after accounting for growth expenses.

At that rate, they need to raise every 18 to 24 months just to stay alive. The funding treadmill doesn’t stop until they either reach profitability or run out of investors.

Dozens of smaller AI startups won’t make it. The ones with single-feature products, weak moats, and high burn rates are dead companies walking. They just don’t know it yet.

A few will get acquired for talent. Most will quietly shut down. We’ll see the wave of closures starting Q2 2026 as Series A and Series B money dries up.

The survivors will be the ones with either strong enterprise revenue or extremely lean operations. Everything in between is squeezed.

Reader Homework – Check Your Own Company

If you work at a company spending on AI, pull these numbers:

- Total AI-related spending in 2024 (include software, compute, salaries, infrastructure)

- Revenue or cost savings directly attributable to AI in 2024

- Number of active AI projects

- Number of AI projects that met their original ROI targets

Compare them. If your spending is more than 5x your returns and most projects missed targets, you’re in the danger zone. Not catastrophic yet. But the clock’s ticking.

Most companies can’t pull these numbers easily. That’s a signal in itself. If you don’t know what you’re spending or what you’re getting, the ROI is probably bad.

Better companies track this monthly. They kill projects that aren’t working. They double down on the ones that are. They treat AI like any other investment–with rigor and accountability.

Weaker companies track it poorly or not at all. They let projects drift. They renew contracts because it’s easier than canceling. They chase AI because everyone else is doing it.

Why NVIDIA Keeps Winning

One company’s making real money. NVIDIA.

Data center revenue for fiscal 2026: $170 billion. Up 65% year over year. Gross margins: 75%. Free cashflow: $128 billion. These aren’t projections. This is happening.

Jensen Huang said at a developer conference they have “visibility to half a trillion dollars in Blackwell and Rubin revenue from the start of this year through the end of calendar 2026.”

Half a trillion. In orders. Not hopes. Actual purchase commitments.

Cloud GPUs are sold out through 2026. Demand for 2027 looks similar. Every hyperscaler, every AI lab, every enterprise with serious AI plans–they all need NVIDIA chips.

The Blackwell platform shipped in Q4 2024. Revenue ramped instantly. By Q3 2025, Blackwell revenue grew 17% sequentially. By Q4, it’s probably 30% of data center sales.

Rubin launches second half of 2026. It’ll deliver 4x the inference performance of Blackwell. Customers are already lining up.

Meanwhile, Microsoft, Google, Amazon, and Meta are all trying to build custom chips to reduce NVIDIA dependence. Google has TPUs. Amazon has Trainium and Inferentia. Microsoft’s working with AMD. Meta partnered with Broadcom.

Hasn’t mattered yet. NVIDIA’s lead in software (CUDA), ecosystem, and performance is too large. Switching costs are massive. Even companies building custom silicon still buy NVIDIA chips for the workloads that need peak performance.

The moat is real. And it’s widening.

NVIDIA’s also smart about partnership. They invested in OpenAI. They’re working with Anthropic. They supply to Microsoft, Google, Amazon, Oracle, Tesla, Meta, and every AI player that matters. When the AI boom pays off, NVIDIA wins no matter who succeeds at the application layer.

That’s the difference between selling infrastructure and selling services. Infrastructure gets paid upfront. Services have to prove ROI. Infrastructure wins.

What Happens If the Gap Persists

Let’s say we get to end of 2026 and the numbers look like this:

- Hyperscaler AI spending: $590 billion

- Attributable AI revenue: $85 billion

- Spend-to-revenue ratio: 6.9:1

That’s better than 2025 but still terrible. Cloud was under 3:1 at this stage.

What breaks?

First, the public markets revolt. Investors stop rewarding AI spending without clear returns. Stock multiples compress. Meta, Alphabet, Microsoft, Amazon all trade down. NVIDIA probably holds because they’re profitable. But the others get punished.

Second, enterprise budgets freeze. If the hyperscalers are struggling to show ROI, smaller companies will cut. CIOs face CFO pressure. AI projects get shelved. Vendors lose contracts.

Third, the startup ecosystem craters. Venture funding dries up for all but the top-tier companies. Series A and Series B rounds disappear. Burn rates that were acceptable in 2024 and 2025 become fatal in 2026 and 2027.

Fourth, talent flows shift. Right now, AI engineers command $300k to $500k compensation. If companies stop hiring, those salaries normalize fast. The gold rush ends. People move to other sectors.

Fifth, the narrative flips. Media starts writing “AI bubble” stories instead of “AI revolution” stories. Skeptics get louder. Believers get quieter.

None of this means AI is over. It means the current spending pace is unsustainable without revenue catching up. Companies will adjust. Spending will slow. Consolidation will accelerate. Expectations will reset.

The technology keeps improving. The economics have to catch up.

The Part We Don’t Know Yet

We’ve tracked the spending. We’ve estimated the revenue. We’ve built models and ratios and predictions.

But there’s a scenario we can’t fully model: what if the AI unlocks something completely new?

Search started as a way to find websites. It became the dominant advertising platform of the 2000s. Google didn’t predict that in 1998. The value emerged as the technology scaled.

Social networks started as college directories. They became trillion-dollar advertising and data businesses. Facebook didn’t plan that in 2004. It evolved.

Cloud computing started as rented servers. It became the foundation for every modern digital business. AWS didn’t know in 2006 that they’d enable the entire SaaS revolution.

AI might do the same. Maybe the current applications–chatbots, code completion, image generation–are just the beginning. Maybe the real value comes from something we haven’t seen yet.

Agentic AI is the obvious candidate. Autonomous agents that handle complex workflows end-to-end. Instead of a human using AI tools, the AI does the entire job. That’s a different magnitude of impact.

If agents can genuinely replace entire job functions–not just assist them–the economics change. A $200,000 annual salary replaced by $20,000 in compute is a 10x ROI instantly. Do that across millions of roles and you’ve justified every dollar of current spending.

But we’re not there yet. Current agents are brittle. They work in narrow domains with heavy supervision. The fully autonomous, broadly capable agent is still theoretical.

Time will tell if that future arrives. And if it does, how fast.

Until then, companies are betting $500 billion-plus on a future that might happen, hoping they’re not too early or too wrong.

What This Means for You

If you’re an executive allocating AI budget: demand measurable outcomes. Set ROI targets before projects start. Kill the ones that miss. Don’t spend for optics.

If you’re an investor: watch the spend-to-revenue ratios. Companies that can’t tighten that gap by end of 2026 are in trouble. NVIDIA’s probably still a buy. The hyperscalers are riskier. The startups are a crapshoot.

If you’re building an AI company: focus on margin from day one. Revenue growth is great. Profitable revenue growth is what matters. If your gross margins are under 60%, you’re going to struggle. If you’re burning more than you’re making, you’re on a clock.

If you’re choosing which AI tools to adopt: pick the ones with clear ROI in under 12 months. Anything longer is a strategic bet. Make sure you can afford to lose that bet.

The money is real. The technology is real. The question is whether the value arrives fast enough to justify the cost.

Right now, the answer is no. Not yet. Maybe soon.

We’ll be tracking this every quarter. The gap will either close or it won’t. By end of 2026, we’ll know which way it went.

Sources: Company 10-K/10-Q filings, earnings call transcripts (Q3-Q4 2025), Goldman Sachs Research, Gartner IT spending forecasts, Deloitte AI ROI survey 2025, MIT State of AI in Business 2025, Bloomberg Intelligence, Vanguard economic outlook 2026, RBC Wealth Management analysis, analyst consensus estimates compiled February 2026.